The Gabler Wirtschaftslexikon defines controlling as: “… sub-area of the corporate management system, the main task of which is the planning, management and control of all corporate areas.” In the context of an agile company, however, controlling has to reinvent itself to a certain extent. In this article, I would like to give a small preview of which approaches already exist and which questions still need to be clarified in the future.

Role of controlling

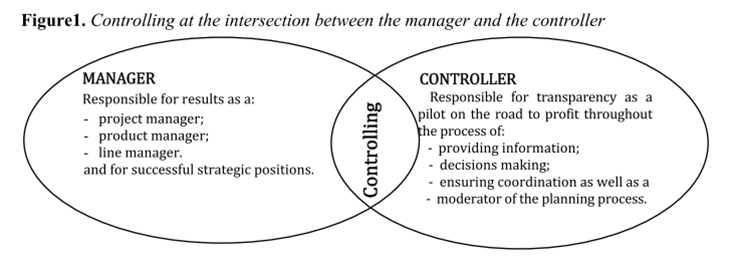

The presentation by Roman et al. (2014, p. 47) clarifies the new role of the agile Controlling. The discipline no longer acts in isolation as a single unit, but acts closely with management. This means that agile controlling in modern, agile companies is not only responsible for precise, customer-oriented reports, but also takes on coordination, moderation and decision-making role that is more oriented towards traditional management than before. Boundaries are softening and the different roles also use methods from other areas.

Hybrid controlling

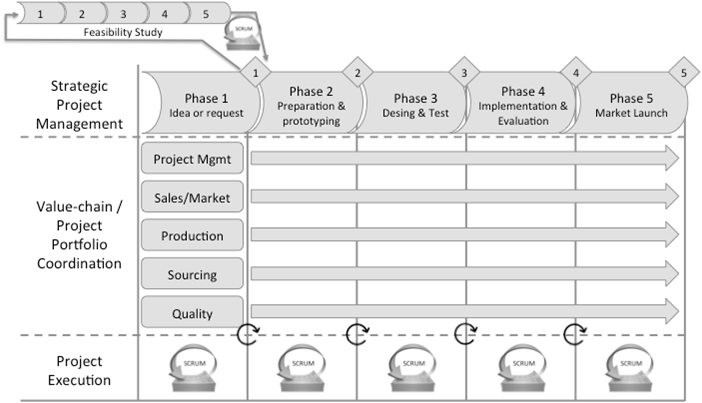

Summer et. al (2015, p. 42) show in this graphic how so-called hybrid controlling is currently becoming the “state of the art” due to the large variety of methods. With this procedure, every single phase of the project is checked by a Qualitygate. Each team is free in the respective phases to use their own chosen methods for the implementation: The spectrum ranges from Scrum to waterfall. With hybrid controlling, controlling is only responsible for tracking the respective results from the phases.

Agile controlling

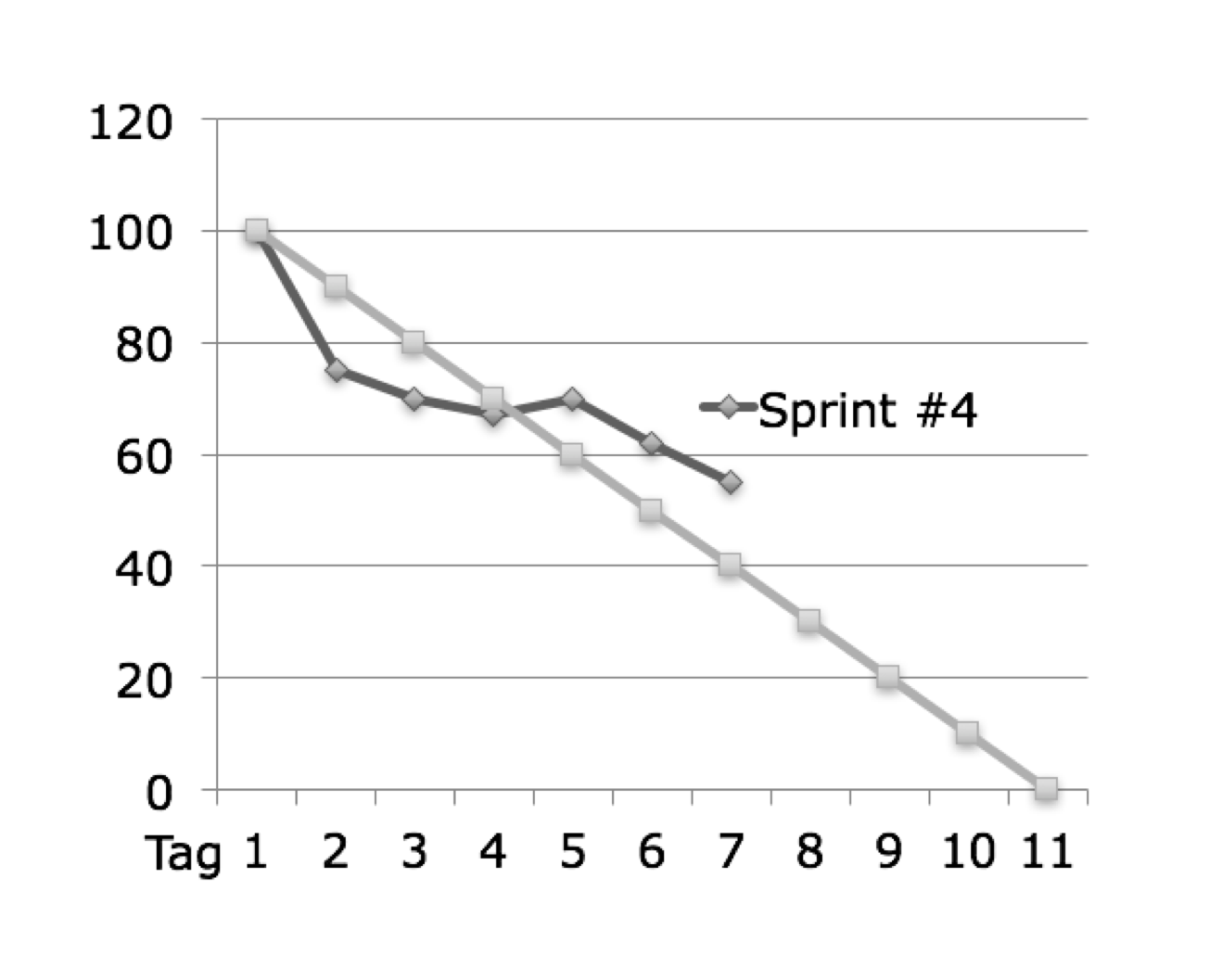

With the implementation of Scrum, controlling has accordingly revealed another task. However, the question arises as to how Scrum can be “controlled” at all. The burn-down chart has an answer: Agile controlling will have the task of establishing such charts within management.

Beyond budgeting as agile controlling

The principle of beyond budgeting plays a further role in controlling. It was developed in England in 1998 and is intended to be a counter-application to “instruction and control” in Taylorism. It is defined by 12 principles, which I would like to briefly address here. For more, see the book: Beyond budgeting – incl. Online work aids: target-oriented management and increase performance without budgets. I have the 12 principles on the Page by Haufe found and would like to quote them here:

6 principles deal with the control process in companies:

- Targets formulated relative to internal or external competition should be self-adjusting and have a performance-enhancing effect.

- Early detection and rolling forecasts should enable constant adjustments of strategy and investment decisions to changed environmental conditions.

- A rolling strategy development and implementation process is intended to promote the strategic coordination of corporate activities. In particular, the balanced scorecard is being propagated as an instrument.

- A flexible allocation of resources should be achieved through the specification of a discount rate by the head office and autonomous decentralized decisions about the investment projects.

- Decentralized units should basically control themselves. The head office only intervenes on a subsidiary basis if the decentralized managers cannot solve a problem or ask for help from top management (“Management by Exception”).

- Relative, team-based compensation that compares the success of the business unit with other units is intended to encourage teamwork and collaboration.

Another 6 principles deal with the organizational framework and corporate culture:

- Leadership through shared values and clear management guidelines should enable quick, decentralized decisions within defined limits.

- Autonomous profit centers should create more entrepreneurship in the company.

- Internal markets for coordinating the profit centers should replace coordination with plans and enable faster reactions.

- Information available everywhere and immediately (“real time”) should lead to the greatest possible transparency and distributed control.

- Freedom of action and decentralized responsibility for results should enable and enforce the performance of decentralized actors.

- A “Coach & Support” leadership style is intended to support the managers in this.

Gloger, B. (2013). Scrum . Munich: Hanser Verlag.

Roman, C., Roman, A.-G., & Meier, E. (2014). The Challenges of Accounting Profession as Generated by Controlling. Theoretical and Applied Economics , XXI (11), 43-56.

Sommer, AF, Hedegaard, C., Dukovska-Popovska, I., & Steger-Jensen, K. (2015). Improved Product Development Performance through Agile / Stage-Gate Hybrids: The Next-Generation Stage-Gate Process? Research Technology Management , 58 (1), 34-44. http://doi.org/10.5437/08956308X5801236